The Quinoa Effect: When “Good Enough” Becomes a Trap

As we know in the early 2000s, Bolivia is highly dominated the global quinoa supply until Western agribusinesses reverse-engineered the crop and undercut Bolivian farmers at every price point. The lesson was brutal and very simple: if you own only the process and not the science of it, you own nothing permanent. India biotech sector stands at precisely this inflection point in 2026. With a $130 billion industry projected to hit $300 billion by 2030, India commands global attention but its celebrated manufacturing muscle is increasingly a double-edged sword. This editorial argues that India must urgently pivot from being the world’s “pharmacy of the south” to becoming a genuine innovation economy, or risk ceding the next biotech revolution to China, the US, and a rising cohort of European deeptech challengers.

What the Numbers Actually Tell Us

The facts, stacked in their most unforgiving order: India accounts for 20% of global generic medicine exports and supplies 60% of the world’s vaccine doses by volume (IBEF, 2026). The Serum Institute of India, led by Adar Poonawalla, remains the world’s largest vaccine manufacturer by output. Dr. Reddy’s Laboratories and Sun Pharmaceutical Industries anchor a generics empire that generated combined revenues exceeding $8 billion in FY2025.

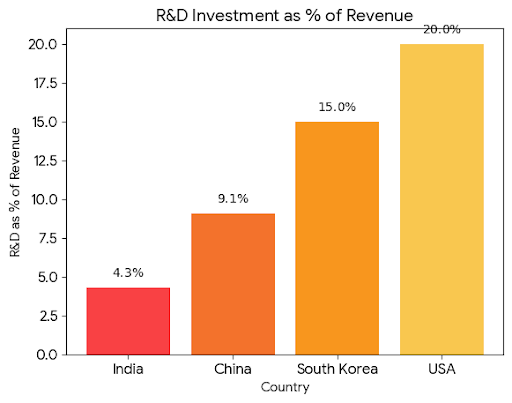

Yet here is the fault line: of the 127 novel molecular entities (NMEs) approved globally in 2025, Indian companies originated fewer than four. R&D expenditure as a percentage of biotech revenue in India sits at 4.3%—compared to 18–22% in the US and 15% in South Korea (Evaluate Pharma, 2026). The Department of Biotechnology (DBT) under Secretary Dr. Rajesh Gokhale has accelerated funding through the BioE3 Policy, committing ₹1,500 crore ($180M) annually a meaningful step, but still a fraction of NIH’s $47 billion annual disbursement.

The Argument: Manufacturing Muscle Is a Depreciating Asset

The global biotech landscape of 2026 is not the landscape of 2010. AI-driven drug discovery, mRNA platforms, CRISPR-based gene editing, and synthetic biology are rewriting who holds structural power in the sector. These are innovation-intensive, IP-heavy domains and India’s current competitive advantages erode rapidly in this environment.

The Data Doesn’t Lie

| Metric | India (2026) | USA (2026) | China (2026) | South Korea (2026) |

|---|---|---|---|---|

| Biotech Market Size | $130B | $890B | $310B | $95B |

| R&D as % of Revenue | 4.3% | 20.1% | 9.1% | 15.3% |

| Novel Drug Approvals (2025) | 4 | 58 | 14 | 9 |

| Unicorn Biotech Startups | 6 | 210 | 87 | 22 |

| Clinical Trial Registrations | 1,842 | 18,400 | 6,200 | 3,100 |

| Patent Filings (Biotech) | 4,100 | 47,000 | 38,000 | 12,500 |

Sources: IBEF, Evaluate Pharma, WHO ICTRP, WIPO — 2026 estimates

India files nine times fewer biotech patents than the United States. More alarmingly, China with a comparable manufacturing base just a decade ago has now produced 87 biotech unicorns versus India’s six. Biocon Biologics, Immuneel Therapeutics, and InvictaBio show the seed of an innovation economy is already present. It has simply been starved of capital, regulatory clarity, and talent retention infrastructure.

The Counterargument—And Why It Falls Short

Critics raise a fair point: India’s manufacturing dominance is not a consolation prize. When COVID-19 vaccines needed to reach two billion people in LMICs, it was Pune that delivered. In a supply-chain-fragmented world, that is geopolitical leverage of the first order.

But this argument, while valid, answers the wrong question. McKinsey’s 2025 Global Biotech Manufacturing Report projects advanced robotics and continuous bioprocessing will reduce the cost advantage of low-wage manufacturing geographies by 35–45% by 2032. India’s moat is evaporating. The question is not whether to protect manufacturing, it is whether India is building the next competitive advantage before the current one disappears.

Solutions: A Five-Point Innovation Agenda

- Triple the BioE3 Budget. Increase to ₹4,500 crore by FY2028, with 40% ring-fenced for basic research at IISc, IIT-Bombay, and CSIR labs.

- Create a Biotech Innovation Exchange (BIX). A SEBI-regulated, NASDAQ-style exchange for early-stage life sciences companies modeled on South Korea’s KOSDAQ biotech board.

- Reform Section 3(d) Patent Law. A nuanced revision, crafted with DPIIT, patient advocates, and industry, can protect public health access while opening viable IP pathways for genuine innovators.

- Launch a National Talent Retention Programme. Over 60% of India’s 12,000 annual life-science PhD graduates emigrate within five years. A structured fellowship with equity participation can reverse this within one policy cycle.

- Mandate Industry-Academia Spinout Pipelines. Tie PLI scheme benefits to co-investment funds with Indian research institutions. A Bharat-Dole model can do for Genome Valley what Bayh-Dole did for Silicon Valley.

📊 What This Means for You

For Investors: Asymmetric returns will come from companies bridging manufacturing scale with novel biologics and AI-driven discovery. Watch Biocon Biologics, Immuneel Therapeutics, and emerging CRISPR startups. The risk premium on Indian biotech innovation is mispriced to the upside.

For Patients: An India that innovates means affordable biosimilars AND domestically-developed therapies for South Asian genetic profiles—TB, type 2 diabetes—where global pipelines remain chronically underfunded.

For Scientists: The window to build world-class careers in Indian biotech has never been wider. The question is whether you wait for the moment or help create it.

The Verdict: Choose the Throne or Inherit the Floor

India’s biotech sector is not at a crossroads. It is at an escalator and the question is whether it rides it up or lets it carry it sideways while the world races past. Foundations are not destinations.

The nations that will dominate biotech in 2035 are making bets today that seem premature, expensive, and uncertain. India has the scientists. It has the infrastructure. It has, increasingly, the capital. What it has lacked is the institutional will to leap from replication to creation from the world’s pharmacy to the world’s laboratory.

That will is now the only thing standing between India and its biotech century.

“The factory floor has served India well. It is time to build the throne.”

Sources: IBEF 2026 Biotech Report; Evaluate Pharma 2025; WHO ICTRP; WIPO Global Innovation Index 2025; McKinsey Global Biotech Manufacturing Outlook 2025; NASSCOM Life Sciences Talent Report 2025; DBT Annual Report FY2025. This editorial does not constitute investment advice.